According to multiple media outlets including CCTV, US President Trump stated at a cabinet meeting held at the White House on July 8 that a new 50% tariff would be imposed on all copper imported into the US, but did not disclose the specific effective date of the new tariff. However, US Secretary of Commerce Lutnick also pointed out on the same day that the Department of Commerce had completed its investigation into copper imports, and Lutnick expected the new tariff "to be implemented possibly by the end of July or August 1." The announcement of this tariff policy had a significant impact on the global copper market. LME copper, SHFE copper, and COMEX copper, which are important indicators of international copper prices, all experienced fluctuations and adjustments. COMEX copper hit a new all-time high of $5.8955/lb during trading on July 8, but then entered a consolidation phase after reaching this peak. As of around 15:32 on July 9, COMEX copper was reported at $5.6135/lb, down 1.27%; LME copper was reported at $9,628/mt, with a decline of 1.66%; SHFE copper fell 1.36% to 78,400 yuan/mt.

》Click to view SMM Futures Data Dashboard

The price spread between COMEX copper and LME copper widened significantly

From the perspective of the price spread between COMEX copper and LME copper, based on the prices around 15:32 on July 9, the price spread between COMEX copper at $5.6135/lb and LME copper at $9,628/mt was $2,747.63, a significant increase compared to the previous spread of around $1,500.

COMEX copper inventories have risen to 220,000 short tons, and copper inventories in non-US regions have also increased

》Click to view SMM Metal Industry Chain Data Terminal

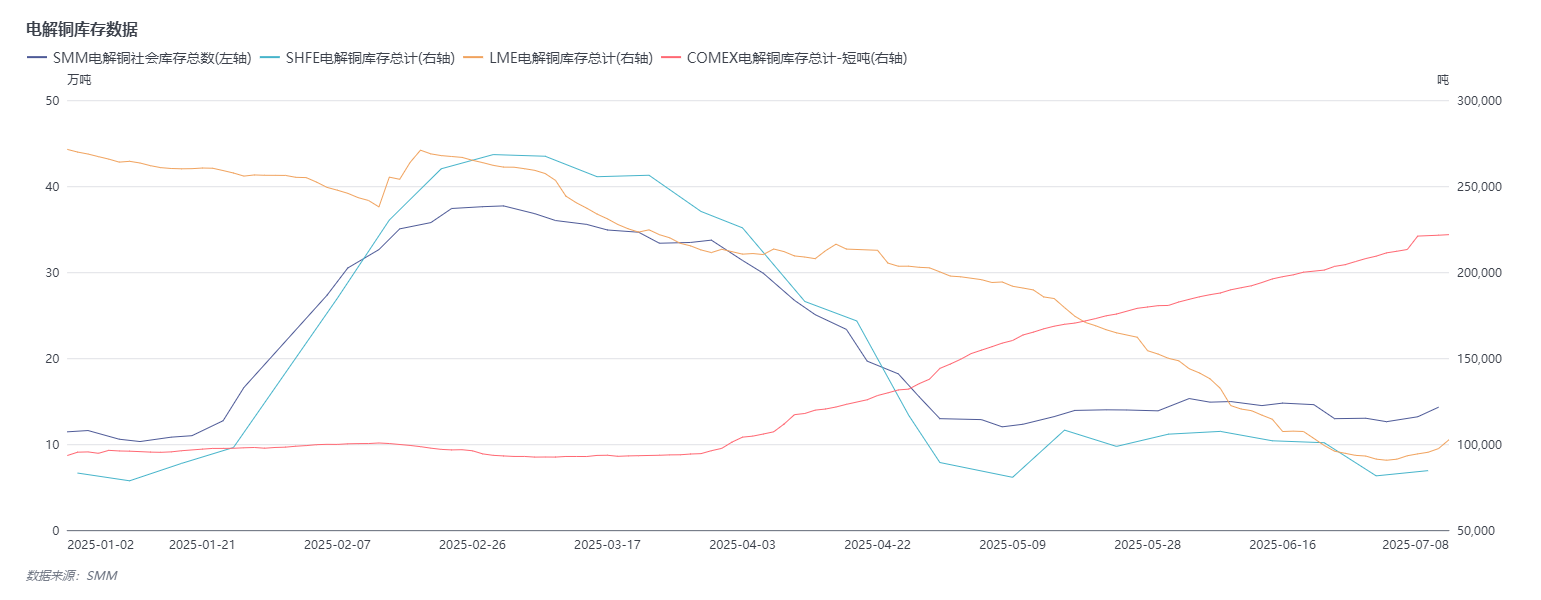

From the inventory data perspective:

Based on SMM's copper inventory data from major regions across the country, as of July 9 (Wednesday), and compared to July 7 (Monday), SMM's copper inventory in major regions across the country increased by 11,100 mt to 142,900 mt compared to last Thursday; compared to the inventory changes from last Thursday, inventories in all regions increased. The total inventory was 255,100 mt lower than the 398,000 mt of the same period last year. Compared to the 126,100 mt of SMM's copper inventory data from major regions across the country on June 3 (Monday), the 142,900 mt increased by 16,800 mt, with a growth rate of 13.32%.

From the perspective of changes in LME copper cathode inventory data, after LME copper inventories fell to a yearly low of 90,625 mt on June 30, LME copper inventories have recently shown a gradual upward trend. The latest inventory data for LME copper inventories as of July 9 was 107,125 mt, an increase of 16,500 mt compared to 90,625 mt, with a growth rate of 18.21%.

From the perspective of COMEX copper inventory data: COMEX copper inventories had risen to 221,788 short tons on July 8, an increase of 10,579 short tons compared to the 211,209 short tons of COMEX copper inventories on June 30, with a growth rate of 5%.

Outlook

Macro Perspective:

Renewed concerns over tariff uncertainties have dampened market risk appetite. COMEX copper prices have surged due to copper tariffs, while LME copper prices have come under pressure due to increased copper inventories in non-US regions. For the outlook, the key variable lies in whether there will be unexpected positive economic data or policy announcements at home and abroad: if a "tailwind" emerges at the macro level, it may offset the downward pressure on copper prices caused by tariffs; otherwise, under the continued disruption of tariff policies, copper prices are unlikely to show outstanding performance in the short term.

Fundamentals Side:

Supply Side: According to data released by the Central Bank of Chile on Monday, Chile exported copper worth $4.7 billion in June, the highest amount since December 2021, with the value increase exceeding the price increase. Although Chile has not yet released its June copper production data, the impressive export figures have been interpreted by the market as an indication of rising copper production in Chile, and the new supply will limit the increase in copper prices in the short term.

Consumption and Inventory Side: Both domestic and imported copper arrivals are expected to increase this week, with total supply expected to rise WoW. In terms of consumption, it is anticipated that consumption will increase this week compared to last week following the pullback in copper prices. SMM predicts that copper will see increased supply and demand during the week, with weekly copper inventories possibly continuing to rise slightly. Meanwhile, there are already signs of increasing copper inventories in China and non-US regions such as LME copper inventories. The proposed timing of the US tariff hike may be earlier than market expectations, further increasing the likelihood of continued inventory increases in non-US regions. The supportive effect of low inventory levels on copper prices has thus been weakened, adding another layer of pressure to copper price trends.

Price Spread Impact:

It is worth noting that the current price spread between COMEX copper and LME copper has widened significantly, and this price divergence is becoming a key variable influencing global copper market capital flows and trade patterns. From a driving logic perspective, the huge arbitrage opportunities created by the short-term widening of the price spread are attracting traders to accelerate the shipment of copper resources from non-US regions to the US market. After all, before the tariff policy is implemented, seizing this time window to complete deliveries can earn excess returns between the price spread and freight costs, which has also led to a phased increase in US copper imports recently.

However, the sustainability of this arbitrage behavior is facing strong impacts from tariff policies. As market expectations for the implementation of a 50% US copper tariff continue to rise (especially with the implementation window from late July to early August predicted by Lutnick approaching), traders have begun to adjust their transportation strategies: on the one hand, short-haul transportation orders that were placed in advance may be completed in bulk before the tariff takes effect, but new orders for long-haul transportation have significantly decreased. The market is generally concerned that after the tariff is implemented, the cost of importing copper into the US will rise sharply, and the cross-market arbitrage opportunities may be eliminated by policy barriers at that time; on the other hand, copper resources originally planned to be shipped to the US are gradually being redirected to non-US regions such as Europe and Asia, which will directly alleviate the price support formed by previous tight supply in non-US markets. For example, the upward momentum of LME and SHFE copper prices previously driven by regional supply tightness may weaken with the increase in resource inflows.

More notably, this shift in trade flows may alter the price spread differentiation between the New York and London markets: the COMEX copper market may face limited price gains due to demand digestion pressure following a short-term influx of resources, coupled with anticipated contraction in imports after tariffs are imposed; while the LME market, though receiving a resource replenishment, may see relatively controlled downside room for price declines considering the limited global copper supply increment and the remaining resilience in non-US consumption, potentially leading to reduced price spread fluctuations between the two markets.

Institutional Perspectives

On July 9 (Wednesday), Goldman Sachs stated that copper export expectations to the US are expected to accelerate in the coming weeks, following US President Trump's announcement of a 50% tariff on imported copper. Goldman Sachs, in its report, raised its estimate for the US copper import tariff benchmark from the previous 25% to 50%. Goldman Sachs maintains its forecast for LME copper prices at $9,700 per mt in December 2025, but currently believes that the risk of prices breaking above $10,000 per mt in Q3 has diminished.

Citi Research analyst Tom Mulqueen stated on July 9 (Wednesday) that Trump's announcement on Tuesday of a 50% tariff on copper may drive LME copper prices below $9,000 per mt. US Commerce Secretary Lutnick indicated overnight that Trump will impose a 50% tariff on copper by August 1 or earlier. The clarity of the tariff implementation timetable is crucial for pricing in non-US markets, which will put an end to the recent phenomenon of substantial spot copper flows from non-US regions to the US. From a 0-3 month outlook, this should drive copper prices in non-US regions back down to $8,800 per mt.

Jinyuan Futures stated: Trump's threat to impose a hefty 50% tariff on imported copper caused a surge in US copper prices during trading, attracting a large influx of cross-market arbitrage funds to suppress LME copper prices. His simultaneous plan to impose new tariffs on pharmaceuticals, semiconductors, and multiple specific industries has sparked market concerns, intensifying uncertainties in the global trade situation. Fundamentals side, overseas concentrate supply remains tight, LME inventories have rebounded from low levels, and the sentiment of short squeezes has slightly cooled. The recent surge in US tariff expectations has exacerbated market volatility in overseas markets. It is anticipated that the volatility of US copper prices will increase, while LME copper prices will experience a short-term downward correction to confirm support levels.

Everbright Futures' research report points out: On the macro front, the market is concerned about the re-emergence of trade tensions, with Trump threatening to impose a 50% tariff on copper. On the fundamental front, LME, COMEX, and domestic social inventories have all seen inventory buildups, with LME inventories showing marginal increases and US copper inventories showing marginal declines, alleviating market concerns about short squeezes amid low inventories. Trump's threat last night to impose a 50% tariff on US copper caused market volatility, with US copper prices recording their largest gain in decades, while LME copper prices fell rapidly. This may imply that the implementation of tariffs will mean that US copper and overseas copper will each bear part of the impact, which remains to be observed. However, if tariffs are implemented, it will also mean that the story of copper inventory migration is nearing its end.

Recommended Reads:

》COMEX Copper Hits Record High Amid US Tariff Policy Disruptions

》Chile, World's No.1 Copper Producer, Monitoring Latest US Tariff Policy Developments

》COMEX Copper Inventories Rise to 221,788 Short Tons on July 8